Is This Asia's Quarter

- Financial Insights

- Market Insights

- Japanese equities were the star of the just-concluded quarter

- US equities, meanwhile, benefitted from strong performances from software, insurance, and energy sectors

- As China stabilises, investors wonder if this could be Asia’s quarter

- US Treasuries receive good support in the final auctions of the quarter, after some lacklustre performance

Gary Dugan, Chadi Farah, Bill O'Neill

The Global CIO Office

Japan led the first-quarter gains in the global equity markets with an 11% return in USD terms. The US was just slightly behind with a 10.3% gain, as surprisingly robust domestic growth aided sentiments. Bonds lagged with near-zero returns and only high yield bonds and emerging market debt were able to eke out decent returns (150 bps) for the quarter.

Despite persisting concerns about high valuations, the US equity market managed to maintain its strength due to some strong performances from sectors such as semiconductors (+34%), insurance (+12%), and energy (+12%). The signals out there are mixed. Aggregate corporate profits are flat lining, interest rates remain high, and the Fed is in no rush to cut rates. Money flows, however, have kept the market in good shape.

Table 1: Key Equity Market Performances in Q1 (Total Returns USD)

Source: Bloomberg

Diversification is key

With such strong gains in Japan and the US, investors may understandably be looking for new avenues and markets to potentially diversify into. Europe turned in good – but not great – performance in the first quarter and may just surprise some with its performance in the second quarter. It does seem that the ECB and UK monetary policy committees could have a clearer path than the Fed on when to cut interest rates. European households retain sizeable pools of savings that could start to find their way into spending if they believe that lower interest rates are at hand. The UK equity market is starting to show some life after a forgettable 2023.

We are not tempted to take profits in Japan, despite the stellar returns over the past year. We remain hopeful that there are further legs to the market’s performance. The recent spate of high wage settlements – the highest in three decades- must shortly inspire some stronger consumer spending growth. The new scheme to encourage domestic buying of the equity market has had some early success. In January alone the domestic flows into equity mutual funds were the highest since 2021.

Asia ex-Japan needs China as its Engine

In the first quarter, Asia ex-Japan equity markets lagged their global counterparts, posting a modest 2% return compared with the double-digit gains in the United States and more than 6% in Europe. This underperformance was largely attributed to the downturn in the Chinese equity market, which concluded the quarter with losses, despite regaining some momentum towards the end.

The broader Asian economy hinges a great deal on a stronger Chinese economy. Recent indicators suggest a potential economic turning point in China, with economic confidence data surpassing expectations. Notably, the Federation of Logistics in China over the weekend reported heightened manufacturing and service sector confidence, exceeding market forecasts. These data points reinforce the good news from the previous week that showed investment and industrial output well ahead of expectations.

‘Betting’ on Macau

Tourism in Macau presents a recovery narrative, with visitor numbers nearing pre-pandemic levels, highlighted by the influx during the recent Lunar New Year holiday. Last month’s Lunar New Year holiday saw a daily average that was just shy of 170,000 visitors – very close to that seen during the same period in 2019, the last full year before coronavirus decimated the tourism industry. Macau’s daily visitor arrivals averaged 92,300 in January, an 84% recovery when compared with January 2019. Macau is an example of a philosophical resetting of the economy’s dynamics. Gone are the days when the focus was entirely on high rollers (who have since been severely affected by the government’s crackdown on the wealthy). Today the city welcomes the gambling masses, which offers almost four times the margin on gross gambling revenue.

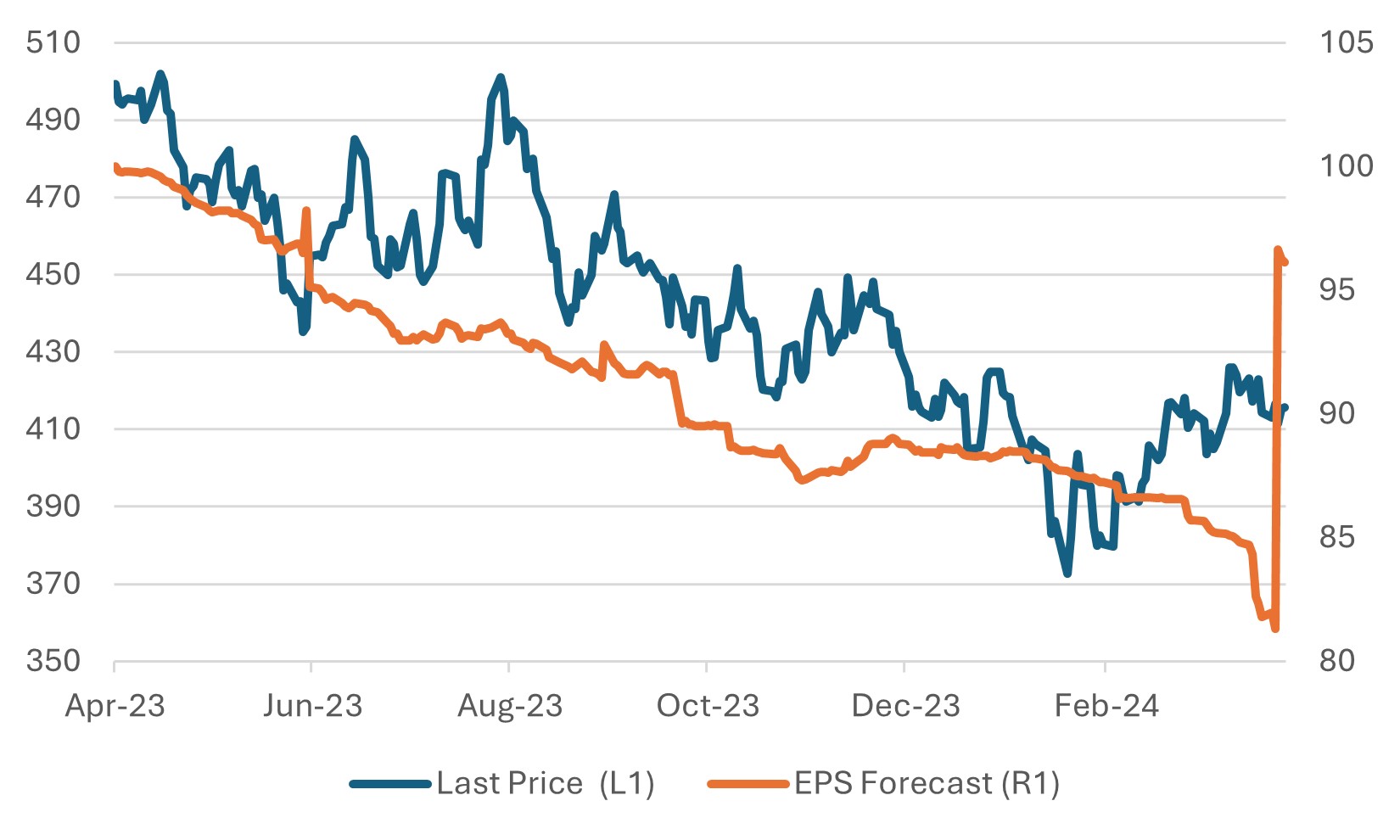

Chart 1: China’s Economic Surprise Index Stable

Source: Bloomberg

We are growing increasingly more confident about our neutral view of the Chinese equity market. In a global context a neutral view is positive given the ongoing debate about whether the Chinese equity market is investable. Our optimism is underpinned by two key observations: firstly, the Chinese authorities have already acted to prevent significant market declines, signalling their reluctance to allow further sharp drops. Secondly, there have been signs of incremental improvements in the economy, reinforcing our long-held belief that a stabilisation in economic data would be a precursor to a market rebound.

Since mid-January, we’ve seen the equity market recover, although it did experience a slight dip in confidence as the quarter ended. The recovery was initially fuelled by governmental interventions at regular intervals that aimed at stabilising the market. We believe the authorities will continue their efforts to support the market, despite ongoing challenges, including the market still trading 10% below its late-2023 level. This underperformance has largely been because of declining corporate earnings forecasts throughout 2023. Nonetheless, there is an expectation of a 15% market recovery in 2024, although this projection is met with some scepticism.

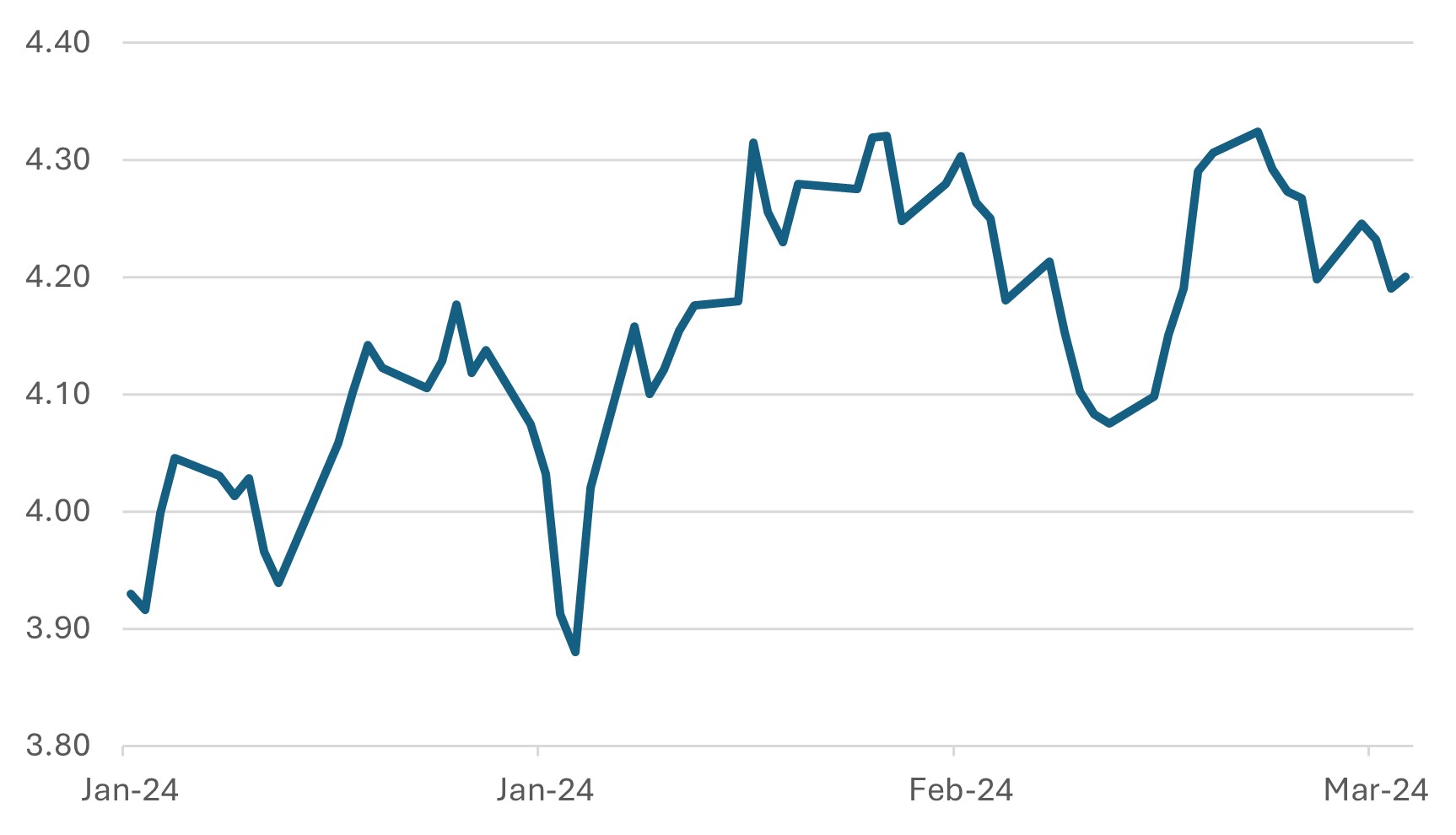

Chart 2: Chinese Corporate Earnings Forecats Could Aid a Recovery in Equities

EPS rebased to April ’23=100, EPS jumps to reflect a data point for the subsequent year

Source: Bloomberg

Bonds – US Treasuries Seeing Support after the Quarter’s Rise in Yields

In the US, the pain trade for asset allocators has been in the bond market. The US 10-year government bond yield has risen 32bps since the start of the year, presenting a headwind to bond returns. Last week’s economic data flow and comments from Fed governors was the same mix of marginally stronger-than-expected inflation data (PCE a tenth above expectations) and the net marginal hawkish tone from Fed governors. The better news for bonds was that there was still good demand at the US government bond auctions in the past week despite the ongoing extraordinary amount of new issuance. After the marked underperformance of bonds versus equities in the past quarter, investors may have belatedly seen some relative value in fixed income!

Chart 3: Rise in US 10-year Government Bond Yield a headwind to Bond Returns

Gross redemption Yield (%)

Source: Bloomberg

Table 2: Bond market returns for Q1

SDAX Investment Deals