- Financial Insights

- Market Insights

When the Good News Runs Out

- Gold – How about $11,000?

- Gold price to M2 money supply ratio shows still more upside

- The yellow metal’s outperformance versus equities is unprecedented, given equities haven’t fallen

- Private Credit has its wake-up call – high-yield spreads widen

- China’s Plenum set to spell out the long-term vision

- France and Japan are still stuck with the challenges of democracy

Gold just keeps scaling new heights, and investors are struggling to find a framework to assess how far it might go. As we marvel at its remarkable advance, we wonder what is gold really worth, and how we should think about its valuation in a world awash with paper money. While those dynamics aren’t that simple to understand, gold’s advance this year does not simply reflect another speculative rally; it details a deeper story about money itself.

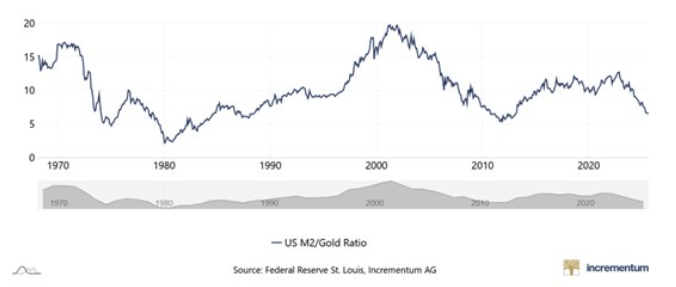

The link between gold and the global money supply, the so-called M2 framework, is one way to understand why there may still be considerable upside. This past week, a savvy contact of mine reminded me of the relationship, which notes that as the supply of money continues to expand far faster than the real economy, the purchasing power of that money inevitably weakens. Gold, by contrast, cannot be printed or manipulated by policy. Over time, it tends to re-price to reflect the cumulative debasement of currencies. Were gold to align fully with the growth in global M2 since the early 2000s, its theoretical value could approach $11,000 an ounce, reflecting a ratio that is more akin to where we were in 1980. That is not necessarily a forecast, but it does show how detached our monetary system has become from tangible value. With central banks creating unprecedented liquidity, governments locked into chronic deficits, and real yields still negative in much of the world, it would be surprising if gold did not continue to rise.

Chart 1: Ratio of M2 Money Supply Growth to Gold

Source: Bloomberg

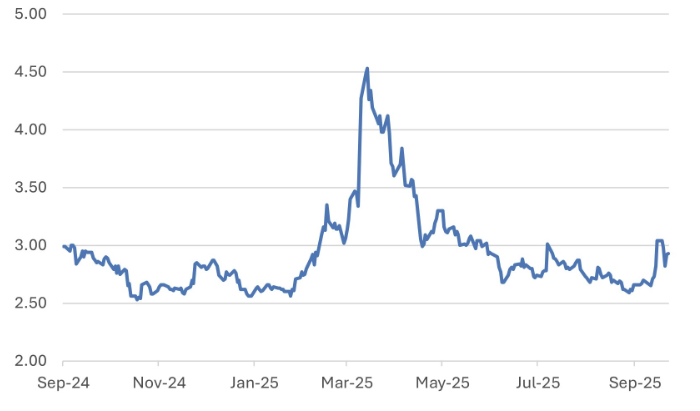

Conventionally, when gold is rising, equities are in trouble. However, what makes gold’s current run so striking is that it has outperformed global equities by around 40% over the past year, one of the strongest relative performances in decades, yet equity markets have remained buoyant (Chart 2). It is a quiet but powerful rebellion on the part of equities. Evidence suggests that such outperformance has occurred only twice before in the modern era, and on both occasions it coincided with equity market declines, not advances.

Gold is not climbing because investors are fearful; it is rising because they are questioning the very foundations of value. For too long, gold was treated as a hedge to be bought only when the world was falling apart. Now it seems to be reclaiming its older role as a cornerstone of long-term wealth — a measure of stability in an age of monetary strain. Perhaps equities are over-extended, with the illusion of endless liquidity sustaining their march. Or perhaps investors are simply rediscovering that in a world built on credit, something finite, something ancient, still deserves its place at the core of the idea of wealth.

Chart 2: Gold’s Extraordinary Outperformance Versus Equities

Gold’s 12-month rolling performance less the performance of equities

Source: Bloomberg

Cracks in Credit

Evidence is mounting that credit stress is beginning to seep through the financial system once again. While the companies at the heart of the current failures are relatively small, those at the receiving end are not. Jefferies and UBS, for instance, have both disclosed meaningful exposures within their private credit portfolios, suggesting that asset managers may have relaxed risk controls as the asset class enjoyed its bull run.

A cluster of corporate bankruptcies, including Tricolor, a large sub-prime auto lender, and First Brands, has already resulted in notable write-downs across regional banks and investment houses. Fifth Third reported a $178 million charge tied to Tricolor’s collapse, while Zions Bancorp admitted to losses linked to fraudulent commercial loans. These are not isolated incidents; they expose weaknesses in underwriting and internal controls that were dulled by years of cheap liquidity.

Across the regional banking system, loan-loss provisions are rising as credit quality deteriorates, and reserves are drawn down. Balance sheets remain under pressure from unrealised bond losses and narrowing margins, leaving little room for error. Once again, some management teams appear to have forgotten that risk never truly disappears; it merely hides until the cycle turns.

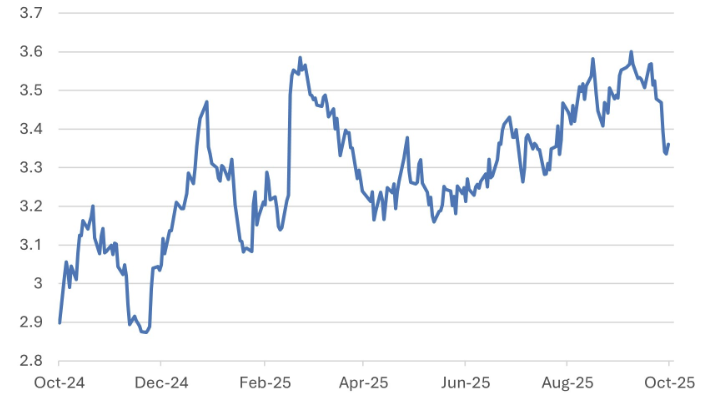

In the broader fixed income markets, there are some signs of strain. High-yield spreads have finally moved to discount less benign conditions going forward. The spread on the Bloomberg Global High Yield index has risen to 293bps from a recent low of 259bps.

Chart 3: Bloomberg US High Yield Index Spread Spikes

Source: Bloomberg

China’s Communist Party Plenum: A Catalyst for Performance from Chinese Equities

The Chinese equity market has had a sharp recovery this year, and we believe there is more upside left. The economy appears to be emerging from a soft patch, and with support from a burst of government spending earmarked for the end of the year, growth could surprise to the upside. More importantly, this week’s Communist Party Plenum is widely anticipated to be a seminal moment for China’s strategic direction, where the blueprint for the next phase of the nation’s development will be hard-coded.

Against a backdrop of global economic uncertainty and perceived political volatility in the US, the Plenum should demonstrate long-term planning and an ambitious vision through the formulation of the country’s next Five-Year Plan. We believe the focus is likely to be on achieving high-quality growth, technological self-reliance, and building a modern socialist country, presenting a stark contrast to short-term political cycles elsewhere. We also expect a clearer articulation of the degree to which China is opening itself up to engagement with the rest of the world.

Democracy’s Challenges

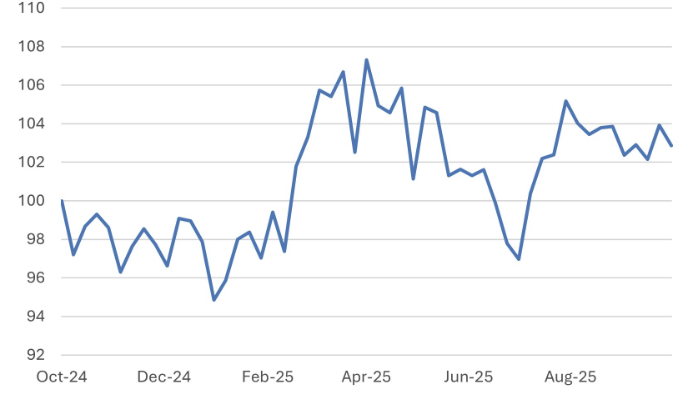

China’s structured long-term planning contrasts with the downside to democracy – phases of political turmoil and possible policy paralysis. In France, Prime Minister Sébastien Lecornu appears to have found a consensus around his second administration in a month to put forward a budget that should carry the day, but challenges lie ahead. The recent rally in French 10-year OATs looks overdone and could be due an unwind to higher yields as political challenges linger.

Chart 4: French 10-year OAT Yield Drops Back, but Appears Vulnerable

Source: Bloomberg

Japan’s political situation remains unresolved, although there are hopes that Sanae Takaichi, the president of the Liberal Democratic Party, can form a government when the Diet reconvenes later this month. Japan’s equity market, at least for the moment, takes strength from ongoing good corporate news as foreign capital continues to come into the market.

Chart 5: Japan’s Equity Market Maintains Relative Strength

Gold’s 12-month rolling performance less the performance of equities

Source: Bloomberg